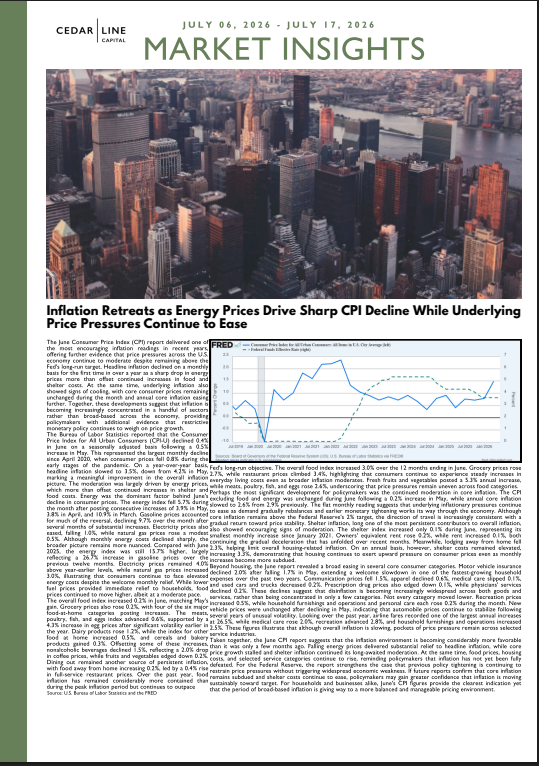

Inflation Retreats as Energy Prices Drive Sharp CPI Decline While Underlying Price Pressures Continue to Ease

U.S. inflation eased markedly in June 2026 as a sharp decline in energy prices pushed headline consumer prices lower for the first time in more than a year. While underlying inflation continued to moderate and shelter costs showed further signs of cooling, persistent increases in food and selected service categories suggest the path back to the Federal Reserve's inflation target remains gradual.

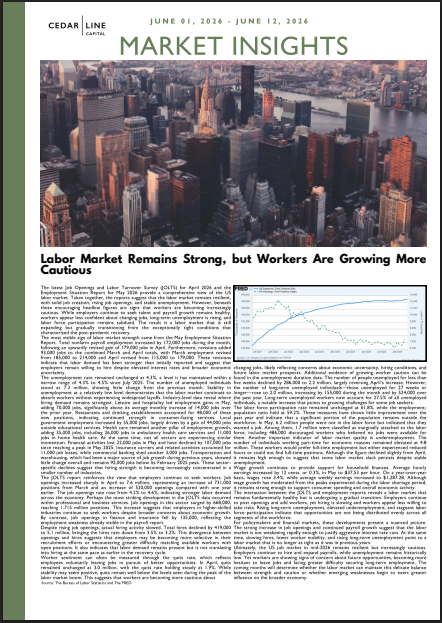

Labor Market Remains Strong, but Workers Are Growing More Cautious

The latest US labor market reports reveal an economy that continues to generate jobs, but with growing signs of underlying weakness. While payroll growth, hiring activity, and wage gains remain positive, rising underemployment, slowing participation, and sector-specific declines suggest that labor market momentum is gradually cooling. This article analyzes the latest data from the BLS, ADP, and JOLTS reports to examine how employment trends are shaping the broader economic outlook and influencing Federal Reserve policy expectations.

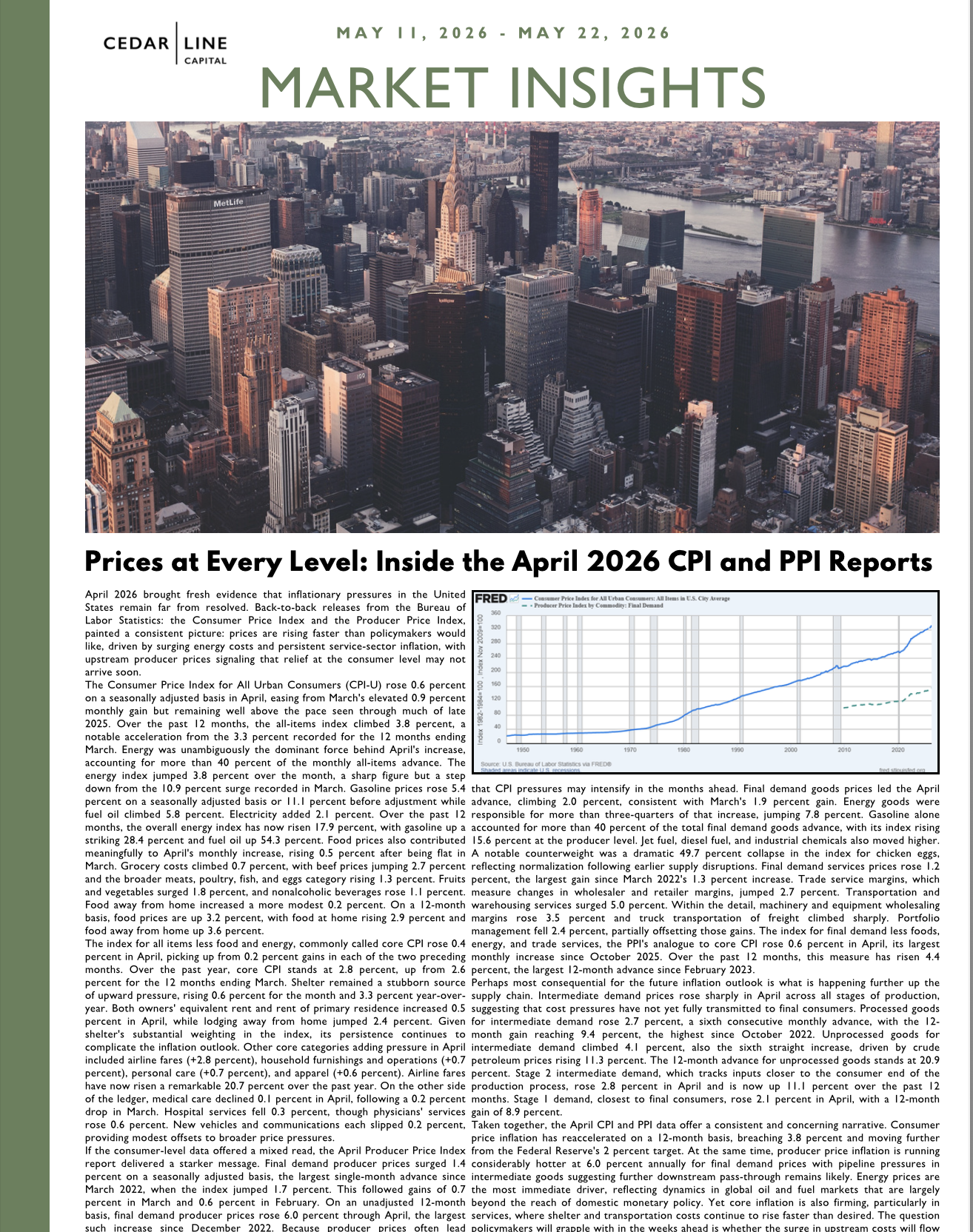

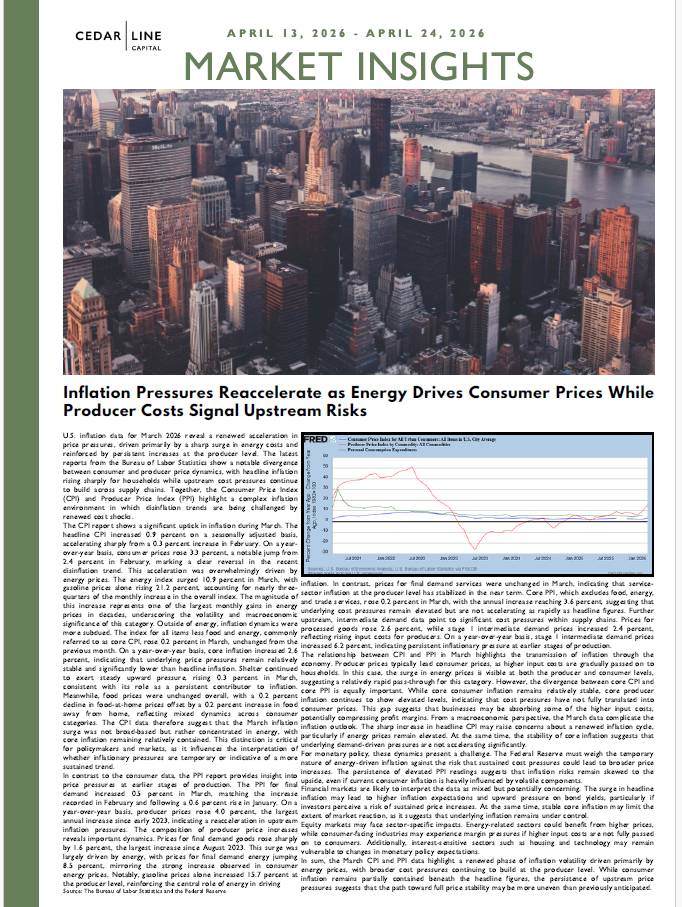

Prices at Every Level: Inside the April 2026 CPI and PPI Reports

The latest US labor market reports reveal an economy that continues to generate jobs, but with growing signs of underlying weakness. While payroll growth, hiring activity, and wage gains remain positive, rising underemployment, slowing participation, and sector-specific declines suggest that labor market momentum is gradually cooling. This article analyzes the latest data from the BLS, ADP, and JOLTS reports to examine how employment trends are shaping the broader economic outlook and influencing Federal Reserve policy expectations.

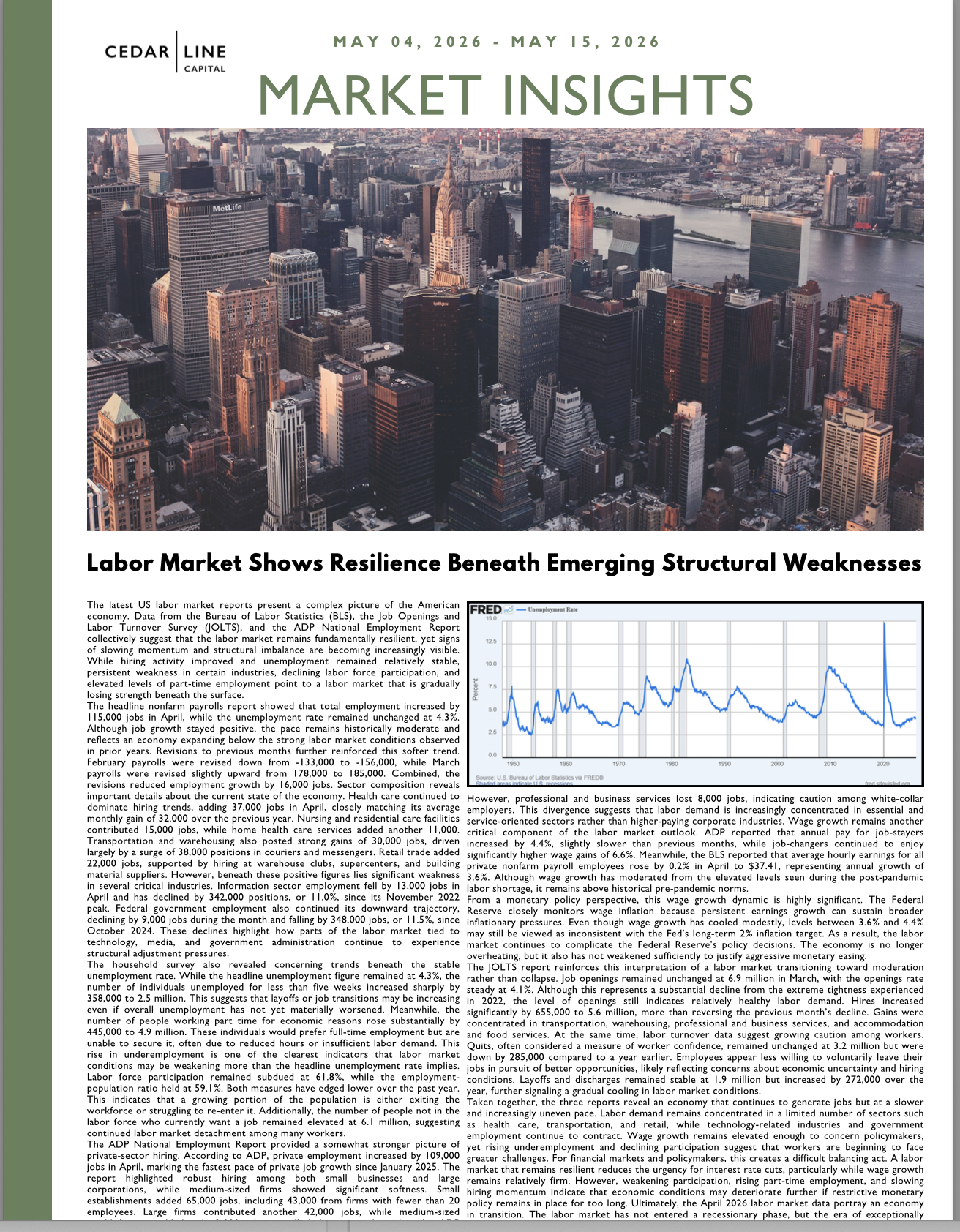

Labor Market Signals Resilience Amid Emerging Economic Pressures

The latest US labor market reports reveal an economy that continues to generate jobs, but with growing signs of underlying weakness. While payroll growth, hiring activity, and wage gains remain positive, rising underemployment, slowing participation, and sector-specific declines suggest that labor market momentum is gradually cooling. This article analyzes the latest data from the BLS, ADP, and JOLTS reports to examine how employment trends are shaping the broader economic outlook and influencing Federal Reserve policy expectations.

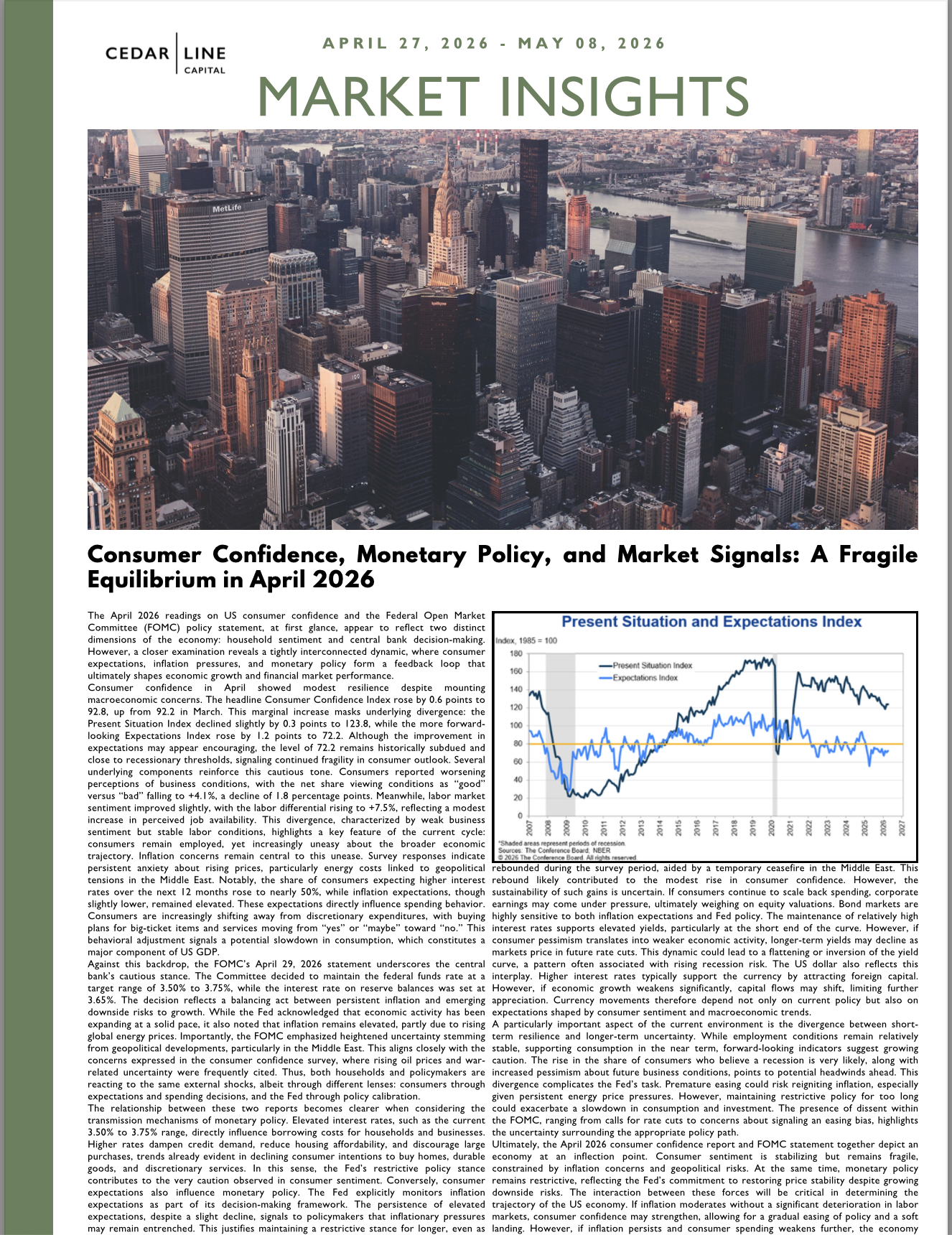

Consumer Confidence vs. Fed Policy: What April 2026 Signals for Markets

March inflation data show a sharp rise in headline consumer prices, driven primarily by a surge in energy costs, while underlying inflation remains relatively contained. At the same time, producer price data point to sustained upstream cost pressures that could gradually feed into consumer prices in the coming months. The divergence between stable core inflation and elevated producer costs highlights an increasingly complex inflation environment. This analysis explores the implications for monetary policy, inflation expectations, and financial markets.

Retail Sales Surge in March as Consumer Spending Remains Resilient Amid Economic Uncertainty

March inflation data show a sharp rise in headline consumer prices, driven primarily by a surge in energy costs, while underlying inflation remains relatively contained. At the same time, producer price data point to sustained upstream cost pressures that could gradually feed into consumer prices in the coming months. The divergence between stable core inflation and elevated producer costs highlights an increasingly complex inflation environment. This analysis explores the implications for monetary policy, inflation expectations, and financial markets.

Energy-Driven Inflation Surge Masks Persistent Upstream Price Pressures in March

March inflation data show a sharp rise in headline consumer prices, driven primarily by a surge in energy costs, while underlying inflation remains relatively contained. At the same time, producer price data point to sustained upstream cost pressures that could gradually feed into consumer prices in the coming months. The divergence between stable core inflation and elevated producer costs highlights an increasingly complex inflation environment. This analysis explores the implications for monetary policy, inflation expectations, and financial markets.

U.S. Consumer Spending Holds Firm Despite Income Declines and Rising Credit Dependence

February data show U.S. consumers continuing to support economic growth through steady spending, even as personal income declined and savings rates fell. The divergence between income and consumption highlights increasing reliance on credit and financial buffers to sustain demand. While inflation has moderated, persistent price pressures and elevated borrowing costs are beginning to weigh on household balance sheets. This analysis examines the sustainability of consumer-driven growth and its implications for monetary policy and financial markets.

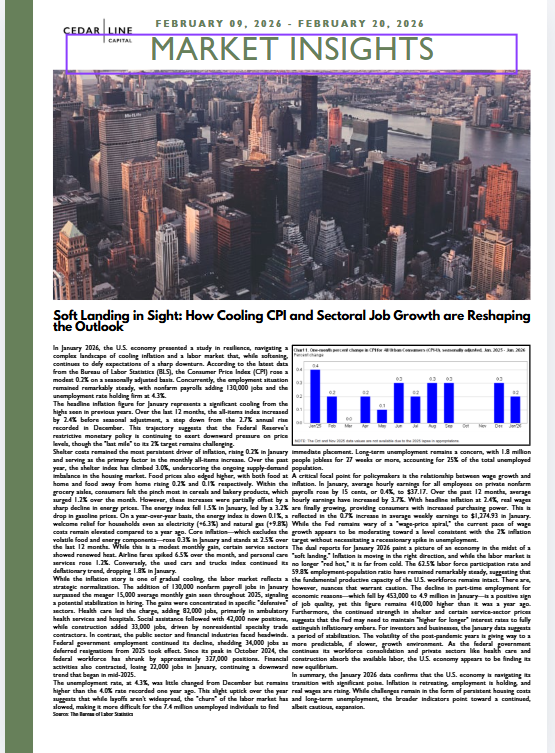

Soft Landing in Sight: How Cooling CPI and Sectoral Job Growth are Reshaping the Outlook

The U.S. economy continues to navigate a delicate transition toward a "soft landing," characterized by a strategic moderation in headline inflation to 2.4% and a resilient, albeit normalizing, labor market. While persistent shelter costs remain a focal point for the Federal Reserve, the addition of 130,000 nonfarm payrolls suggests that the domestic engine is finding a sustainable equilibrium rather than a downturn. Our latest report provides a comprehensive examination of these shifting macroeconomic indicators and their implications for the 2026 fiscal outlook.

January PMI Data Signal Continued Expansion Across the U.S. Economy

U.S. economic momentum improved at the start of 2026, as January PMI data showed manufacturing returning to expansion while services activity remained firmly in growth territory. A rebound in new orders and production points to strengthening demand conditions, even as employment and cost pressures show signs of moderation. Together, the surveys suggest the economy is stabilizing rather than overheating, supporting expectations for steady growth under still-restrictive financial conditions.

Easing Inflation at the Factory Gate Meets Growing Caution Among Consumers

The latest U.S. data show producer price pressures continuing to ease, reinforcing progress in the broader disinflation process. At the same time, consumer confidence has declined, reflecting growing caution among households despite a resilient labor market. This divergence highlights the late-stage dynamics of monetary tightening, where inflation cools faster than sentiment recovers. Our analysis explores what these trends mean for demand, pricing power, and the economic outlook.

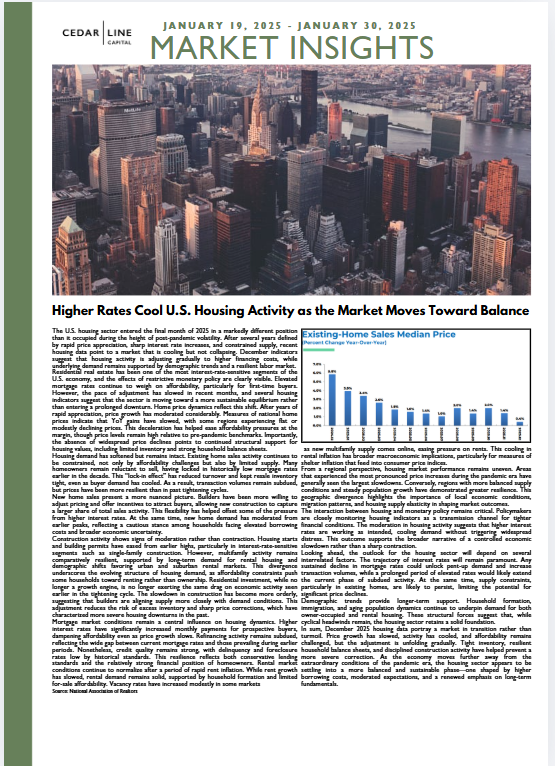

Higher Rates Cool U.S. Housing Activity as the Market Moves Toward Balance

The U.S. housing market is finally finding its footing. While higher interest rates have taken some of the heat out of demand, they haven’t sparked the kind of sharp correction many feared. December’s numbers tell a story of cooler, but more balanced, conditions: slower price gains, softer sales volumes, and a gradual reset between buyers and sellers. Limited inventory and generally healthy household finances are keeping a floor under prices, even as affordability remains a challenge. In our latest report, we break down what this shifting landscape means for housing activity and the broader economic outlook as we head into 2026.

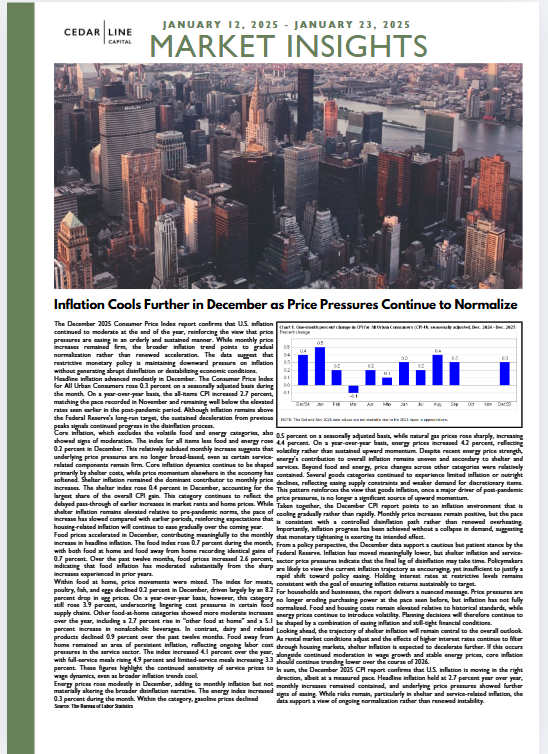

Inflation Cools Further in December as Price Pressures Continue to Normalize

The December CPI report confirms that U.S. inflation is cooling in a steady, well-managed fashion. Headline inflation is holding at 2.7% year over year, and the underlying price pressures that worried markets earlier in the cycle continue to ease. While shelter and other services remain relatively expensive, price growth for goods has slowed meaningfully and month‑to‑month increases are staying in check. Taken together, these trends point to a Federal Reserve policy stance that is successfully cooling the economy without knocking demand off course. In our latest note, we break down the main forces shaping December’s inflation data and what they could mean for the next phase of the inflation and interest rate story.

U.S. Credit and Labor Markets Cool in Tandem as Policy Restraint Takes Hold

The latest U.S. data on consumer credit, employment, and job openings point to an economy slowing in a controlled and deliberate manner. Household borrowing is moderating, labor demand is easing, and wage pressures continue to soften without signs of acute stress. Together, these developments suggest monetary tightening is restraining demand while preserving overall economic stability.